Alberta Women $532,640 in Hole After They ‘Failed to Do the Math’ on Real Estate Investments

Andrew Allentuck

Situation:

Couple has heavy debt from purchase of rental properties that are draining their finances

Solution:

Reduce debt and portfolio risk, then sell remaining cash flow negative property, even if it means a loss

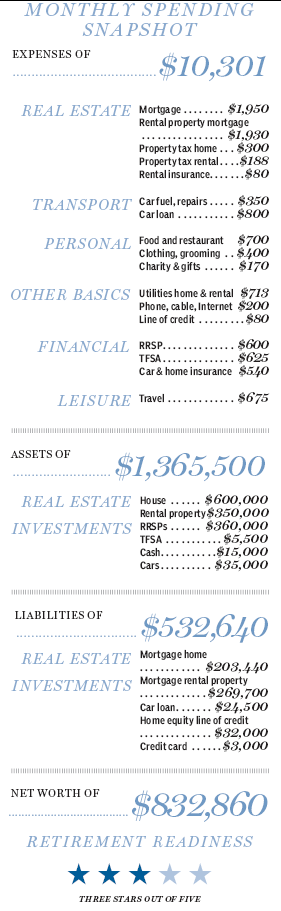

In Alberta, two women – we’ll call them Georgia, 60, and Ruth, 57, have built their lives on two successful careers. Together for three decades, they have owned their own home for 20 years. They have take-home salary income of $10,651 a month based on Georgia’s job as manager of a pubic relations business and Ruth’s as a civil servant. It looks like a financially solid dual career household, but debt left over from a bad real estate investment is a cloud on the horizon.

They have more than half a million dollars of liabilities — $532,640, to be exact — $203,440 of that is secured by their home, $269,700 by a rental property, $32,000 is for a line of credit, $3,000 is on a credit card and $24,500 is a car loan.

“The couple lost their focus, bought rental properties at peak prices and now have to paddle upstream and delay their retirement,” he explains. “They failed to do the math before they took on a huge obligation, but it’s possible to get back on course to retirement with a five-year plan.”

The process will be debt management and portfolio risk reduction. In the end, the debt will be gone and they will have ample retirement income.

Their biggest debt is a carryover from a rental property speculation gone sour. In 2007, Georgia and Ruth borrowed against what was then their mortgage-free home to buy two rental properties. Their total loan was $895,000. That broke down to a $285,000 mortgage on their home and $610,000 against the rental units.

One of the rental properties had bad tenants, then no tenants. Both were running at a loss. So they sold one last year and took a $115,000 loss in Alberta’s volatile real estate market. Now they have to deal with the remaining debt and the residual line of credit.

The remaining rental property initially cost them $450,000 for purchase and some repairs. Today it is worth an estimated $350,000, but it has stable renters who pay $2,350 a month. They want to keep the unit and hope that in a few years they can get their $100,000 price difference back. For now, they are carrying the unit at a loss on book value and a loss on rental income, which is $336 a month less than interest they pay and property tax.

Should they sell assets, such as those in their $360,000 RRSPs to pay off debt or keep the RRSPs intact and avoid the high marginal taxes? Or is it a better strategy to keep the debt and pay it down gradually? Their budget is pretty well eaten up by paying their own home mortgage, the usual costs of a moderate lifestyle, $675 a month for travel expenses, and an $800 monthly car loan payment.

Reducing Debt

The first move should be to use a $15,000 tax refund — generated by the money-losing sale of the first property — to pay off their most expensive debt, $3,000 on their credit card, which has a 20% interest rate. The strategy is to use their after-tax dollars to pay down after-tax debt service costs. They can keep paying the mortgage on the money-losing rental property.

Once credit card debt is gone, they can use the $12,000 balance of their cash to eliminate half of their car loan. The balance of the car loans will be paid in 17 months. That will free up $800 a month interest which, in turn, can be added to pay down the $32,000 line of credit. At $800 a month plus the $80 of interest they already pay, the line of credit will be paid off three years later. At that point, they will be 65 and 62.

The rental property brings in $2,350 a month and costs $2,686 to carry for its mortgage, property tax, insurance and utilities. The difference, $336, is their loss. Even if they shifted that cost to their tenant, the property would be a break-even asset on the income statement and able to appreciate or perhaps not in the volatile Alberta market. Interest on the rental mortgage, 5.44% at present, may rise before they sell it, increasing their loss. The mortgage has a remaining amortization term of 18 years. If they did sell, they would book a $100,000 capital loss but save $4,032 a year in rental losses. The future of Alberta property prices is a toss up.

The conservative move is to cut their losses when they can, especially as Georgia and Ruth have discovered that though they wanted to make money, they are not so comfortable being landlords.

In fact, the property is unlikely ever to be a good investment. They are not making payments on their line of credit other than the interest. The value of the rental property is $350,000 and the combined mortgages – home and rental property — is $473,140. The difference is $123,140. They are paying their two mortgages at $46,560 a year, nearly $26,000 of which is principal reduction. In 4 ½ years, difference will be closed and they can sell the rental unit, clearing the debt. There will be transaction costs for selling including commissions and legal fees, but they should be free of all debt at ages 65 and 62, respectively. Their TFSAs could be kept intact as a form of cash savings.

Retirement Planning

These projections suggest that the women will have to keep working in order to generate income to pay down their debts, delaying their retirements for perhaps five years. However, when their debts are eliminated, they will have two full Canada Pension Plan benefits of $12,460 each, two Old Age Security payments of $6,619 each, a $40,800 job pension for Ruth and, assuming 3% growth for five years of Georgia’s $360,000 RRSPs and payout of all income and assets in the following 30 years, $22,625 of potential RRSP income. The total, $100,583 in 2014 dollars, would be fairly evenly divisible. If pension income and other credits are applied, the women would have an 18% average tax rate and take home monthly income of $6,940 a month, which would be more than current spending once their debt service and rental property management costs and retirement savings are eliminated.

“Holding the rental unit until they have paid down their debt enough that the unit’s sale will clear what they owe has risk,” Mr. Moran says. “The market price could continue to fall. But their growth in equity would eventually catch up. With patience, the women can pay off this bad investment and then have a secure retirement.”

(C) 2014 The Financial Post, Used by Permission