Mutual Funds Came Through for this Couple, When the Job Didn’t

Andrew Allentuck

A couple we’ll call Karl and Gabrielle have an enviable life in British Columbia. At the ages of 53 and 58, they have a character home with a price tag of $812,000 and a gross income of $12,940 a month based on Karl’s work as a mechanical engineer and Gabrielle’s as a health care consultant.

How did your mutual funds perform?

Time for a change, or doing just fine thank you — Financial Post crunches the numbers on your investments in our exclusive review

Their goal is an active retirement with lots of travel to begin when Karl is no later than 65. And they hope to have $85,000 after tax to do it with.

For now, their monthly after tax income is $9,655 a month. That income will soon plummet, however, for Gabrielle has lost her job in a corporate shuffle that will see her get her last paycheque in April this year. Her monthly income of $3,600 a month before tax will have ended, leaving Karl as the sole breadwinner.

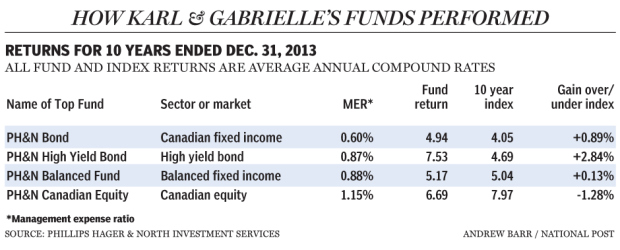

A critical support is going to be their mutual fund investments which have been among the best of their breed.

“We have a portfolio that was set up with what was a hefty load of mutual funds we bought as much as a decade ago beginning in September 2004. That period shows how unexpectedly well our funds did,” Gabrielle says. “I knew that fees mattered from our own negative outcomes with other funds, so the low fee funds we bought were attractive. I was also hoping that by hiring a manager for my money in the funds, I would do better than the market averages.”

Today, those averages are packaged as index funds. But it is not always appealing to buy just average performance or to buy an inadequately diversified index in which one firm or subsector dominates the index, as Nortel Networks did a decade and a half ago when its capitalization accounted for a third of the value of all stocks on the Toronto Stock Exchange.

Karl and Gabrielle invested in funds managed by Phillips Hager & North. Its balanced fund returned 5.17% a year compounded annually for ten years to the end of 2013 compared to 5.04% for its index. Its bond fund delivered 4.94% a year compounded annually compared to 4.05% for its index. The couple’s high yield bond fund scored 7.53% compounded annually beating its index which grew at a comparatively slow rate of 4.69% to the end of December 2013. Finally, their PH&N Canadian equity fund turned in a 6.69% average annual compound return for 10 years ended Dec. 31, 2013, not bad, but less than the 7.97% return of its index. Not every pick turned out to be an index beater.

Yet the group as a whole did well. The reason can be attributed to low management costs well below average for the mutual fund categories they chose, and the ability of the funds’ managers to sell assets vulnerable to problems they saw coming.

Says Nigel Roberts, head of Bluenose Investment Management Inc. in Lake Country, B.C., a chartered financial analyst who manages portfolios for clients, “active managers can tailor portfolios to their outlook for the markets. If they see good things ahead for some stocks or sectors, they can increase their weights of those assets in their portfolios and if they see trouble coming, they can sell those assets, rebalance or stay in cash for a while and stay out of harm’s way.”

It’s the loss of Gabrielle’s job that makes timing retirement critical. Derek Moran, head of Smarter Financial Planning Ltd. in Kelowna, B.C., was enlisted to work out a plan.

“The couple has a dilemma,” he acknowledges, “but in what amounts to accelerated retirement for Gabrielle, there are opportunities.”

Their funds’ ability to generate gains tax free will compensate for much of Gabrielle’s loss of income. Payouts from the RRSPs will incur tax, but that will be over a period of decades as late as the time when they are in their 90s with the partner first to die making the survivor the beneficiary of his or her RRSPs, Mr. Moran notes.

The couple has $596,544 in their RRSPs and $51,649 in TFSAs as part of their approximately $1.4-million financial assets. The balance is cash from recently sold investments and stocks held outside RRSPs.

If Karl works another 12 years to his age 65 with savings stopped due to Gabrielle’s loss of income, then, assuming that all assets grow at 6% less 3% for inflation, at his retirement, they would have $850,500 in their RRSPs and $1,145,000 in the remainder of their financial assets. Karl would then retire, according to his plan.

If at that point they begin to spend the total of their RRSPs, non-registered investments, TFSAs and cash, $1,996,000 in total, growing at 3% a year for 25 years to Gabrielle’s age 95. They would have pre-tax investment income of $111,287 a year.

Added to their estimated CPP income, about 90% of the maximum $12,460 for each person or $22,428 a year combined and Gabrielle’s $6,618 OAS income at 65, and, when he is 66, Karl’s $6,618 OAS, they would have total annual pre-tax income of $146,950.

After splits of eligible pension income to $73,462, a little over the $71,592 OAS clawback trigger in 2014, and payment of tax at an average 38% rate which approximates the total of regular taxes and the clawback, which takes 15 cents of each dollar over the trigger, they would have about $91,100 a year to spend, which exceeds their $85,000 target after tax retirement income. Sustained growth of their investments in mutual funds will have made it possible.

(C) 2014 The National Post, Used by Permission