A Real Estate Crisis in the Making for Couple with $2M Net Worth and not a Stock or Bond to be Seen

Andrew Allentuck

To get to $100,000 post-tax income, they will have to restructure their business assets, which are almost entirely in residential and commercial rental property.

Situation: Couple with $2-million net worth without a single stock, bond or mutual fund looks for $100,000 annual retirement income and early retirement

Solution: Sell one of two properties, invest six figures gain, work to 65. Unless the properties can’t be rented, then things could turn tragic

An Ontario couple we’ll call Frank, 56, and Martha, 52, earn $36,000 a year annual pre-tax income. It’s far less than the $200,000 they made each year for the last two and a half decades in their management consultancy.

A serious car accident left Martha unable to work in the business, which they had to shut down. Today, Martha is a home-based fashion consultant, Frank a manager of building services. Their goal – build a $100,000 after-tax retirement income in the four years they plan to work until retirement. Within a few years, their daughters, who live at home, will have their university degrees and be independent.

But the couple has almost all their money in two real estate properties draining them at a rate of $72,600 a year – twice the income they currently earn.

“Our goal in the next four years is semi-retirement,” Frank explains. “Can we attain $100,000 a year to live on until Martha is 95?”

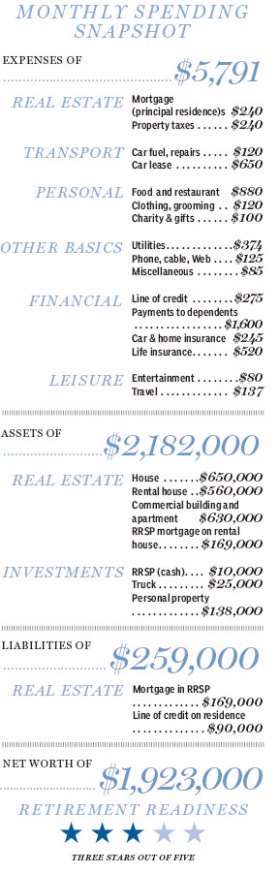

To get to $100,000 post-tax income, they will have to restructure their business assets, which are almost entirely in residential and commercial rental property. They have two rental properties with three units: a commercial property with a store and, as well, an apartment above, and a rental house. To pay the costs – interest, taxes, some utilities and insurance, they spend $6,050 a month. None of the properties is leased. Add in their $5,791 monthly personal expenses and they are spending $11,841 a month or $142,092 a year, extending their line of credit.

If they are successful in leasing all three the properties, they will have gross rents of $105,600 a year. Add in their $36,000 combined salaries and they would have $141,600 pre-tax income. Their rental plus personal living costs would be $142,092. They would be very close to break even but able to generate no savings.

Family Finance asked Derek Moran, head of Smarter Financial Planning Ltd. in Kelowna, B.C., to answer the question as to whether the properties can be a profitable business. His view is a tentative yes, but getting from present earned income of $36,000 a year to the low end of six figures in retirement will require diligent restructuring of their assets. They will have to migrate from subsidizing their rental properties to increasing their cash income and diversifying assets.

A Robust Balance Sheet Supports Meagre Income

“They are asset rich and cash poor,” Mr. Moran says. “They have $2,182,000 in assets. All but $173,000 of that is real estate in one form or another. There is not one stock or mutual fund or bond. They have no tax-free savings accounts. But their net worth is $1,923,000 and there is room and means for distilling it into retirement cash flow.”

Rental one has two parts: An apartment which should bring in $1,400 a month or $16,800 a year. It is above the commercial space which can rent for $5,000 a month or $60,000 a year. The sum of rents for the apartment and the commercial space would be $76,800 a year.

Getting that return is the problem, for though it should happen on paper, neither the apartment above the commercial space, which has been designed for specialized food processing, is rented. Apartments above commercial spaces are not seen as very desirable and can be hard to rent. The commercial space itself needs a very special kind of tenant. In spite of expending a good deal of effort, the couple have not yet found tenants. If the spaces get rented, cash flow will soar. If not, Frank and Martha have many choices including reconfiguring the commercial space. Time is on their side, for they have $1.9-million net worth. It could support a quarter century of vacancy before they are completely broke. But their balance sheet should not be supporting a cash drain, the planner notes. And in due course, chances are that they will be rented.

Rental two, also not rented, is a four-bedroom house that can rent for $2,400 a month or $28,800 a year. The property is valued at $560,000, but its net rental income after deduction of $10,428 in interest, taxes and utilities is $18,372 a year, which is a 4% yield on its $380,000 cost or 3% on $560,000 current value. It’s an inferior investment which should be sold. There would be capital gains tax, but the couple’s present income is low, their tax bracket modest and this year would be a good time to sell, Mr. Moran suggests.

Sale of rental two would bring $560,000 current estimated price less $380,000 which they paid to buy it. Their gain would be $180,000 less estimated tax of $41,400 and $20,000 in real estate and legal fees. That would leave $498,600 cash. They could then pay off their $90,000 line of credit used to finance their current income shortfall and walk away with $408,600. If that sum were invested to yield 4% before inflation, it would produce $16,344 a year before tax with much less risk and much more liquidity than the rental properties.

This rearrangement of assets would leave them with $58,260 in rental income plus their present $36,000 present business income plus $16,344 return on cash from sale of rental two. The sum, $110,604 would achieve their $100,000 pre-tax retirement income target and then some. After 22% average tax, they would have about $7,200 a month to spend.

In time, they could cut many expenses including $275 a month on their line of credit used to finance rental two. When their liabilities are paid off, they could cut $520 in life insurance payments which cover those debts. When their two adult children have finished their post-secondary educations in two years, they could end $1,600 monthly payments to them. Add in food and sundries and their present living costs could drop to perhaps $4,000 a month. They would be able to save perhaps $3,000 a month.

Assuming that they scrap the plan to retire at Frank’s age 60 and instead use the nine years to Frank’s retirement to build capital, then, assuming a 4% return after inflation, they would have $396,220 in financial assets at his age 65. If that sum continued to grow at the same rate with all capital and interest paid out in 34 years to Martha’s age 95, it would generate $20,700 a year.

At Frank’s age 65, when the couple’s retirement would begin, they would give up the $36,000 annual family business income but add $20,700 for the next 34 years, cash from sale of rental two, $16,344 a year, and rental income of $58,260. That’s a total of $95,300 a year. Add Frank’s estimated Canada Pension Plan benefit, $6,230, and his Old Age Security benefit, $6,704 in 2014 dollars, and they would have an annual total of about $108,240 before tax or about $88,760 after 18% average tax. That would be close but not quite at their $100,000 after-tax income target. They could postpone some expenses for a few years and get by or perhaps do a little part time work to the time Martha is 65, the planner suggests.

When Martha is 65, she could begin Canada Pension Plan benefits of an estimated $6,230 and at 67, she could begin OAS benefits of $6,704 a year for sustainable total family income of about $121,200 before tax.

“The subsidies that this couple are pouring into their unrented properties will certainly erode their capital and their way of life,” Mr. Moran says. “The other property – apartment and commercial space – will have to go if they cannot be rented. It’s that or make a slow slide into poverty.”

(C) 2014 The Financial Post, Used by Permission