With $7,000 a Month Going To Service Debt, Future Bleak Unless Couple Can Stem the Red Ink

Andrew Allentuck

Situation: In mid-60s, a couple faces collapsed property investments with scant savings

Solution: Sell last rental property, use money to cut home mortgage and slash other debt

In Alberta, a couple we’ll call John, 65, and his wife, Linda, 66, are on the verge of retirement. John works for a large manufacturing company, Linda for a local non-profit counselling group following an earlier career in health care. The transition to retirement ought to be smooth, but debt and disorganization stand in the way. Their job pension and the Canada Pension Plan will keep a roof over their heads, but their future is paradoxically fragile. They have scant financial assets and a rental property that will lose money when mortgage interest rates rise.

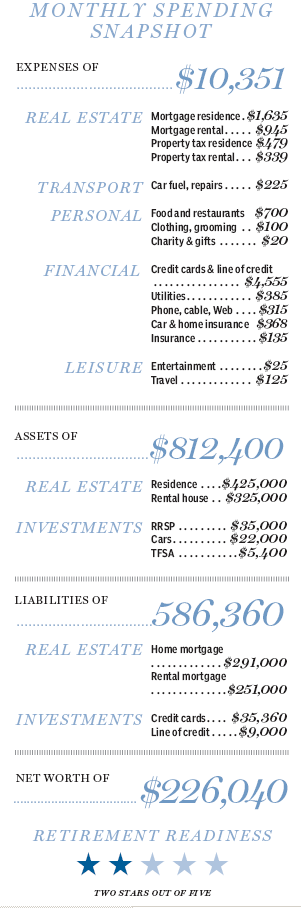

For now, John and Linda are able to keep up with current expenses which include $2,398 in spending each month for groceries, car expenses, grooming, etc, $818 a month in property taxes and a staggering $7,135 a month for debt service on their seven credit cards, line of credit and mortgages. That adds up to $10,351 a month or $124,212 a year. Debt service costs are about 70% of total spending. Their $9,027 monthly disposable income based on their take home salaries, $7,094, and $1,500 monthly rental income, adds up to $108,128 a year. They carry their deficits on their line of credit. But the future is bleak unless they can pay off their debts and staunch the red ink.

“This case is a mess, largely because of the amount and type of debt on their balance sheet,” explains Derek Moran, head of Smarter Financial Planning Ltd. in Kelowna, B.C. “As it stands now, they cannot afford to retire. But we can fix it by debt management first and asset management second.”

Debt Management

The first move has to be to deal with credit card and mortgage debt, for interest rates, as much as 19.9% on their plastic and up to 4% on the mortgages and line of credit are likely to rise. They owe $44,360 on credit cards and line of credit. They have a $291,000 mortgage on their house with a 4% interest rate for another two years and a $251,000 mortgage with a 2.5% floating rate on a rental property.

The couple’s history of investing in real estate ventures is a string of misfortunes. At one time, they owned 12 rental properties, using growing equity in a succession of condos and single homes to provide down payments for the next purchase. But timing purchases and sales and getting enough rent in the notoriously volatile Alberta property market made it hard to manage the dozen profitably, John recalls. Two years ago, they sold all but two properties. Along the way, John had to tap $50,000 of RRSP assets and pay taxes on withdrawals for cash he needed to pay expenses for the properties. Problems with maintenance and tenants not paying rent produced anxiety and health problems. They lost a rental property in a recent foreclosure. One unit remains, a house which makes a small profit. Today, the most expensive debt the couple has is on their credit cards.

Debt management should begin with $35,360 credit card debt which has an estimated interest cost of about $7,000 a year. They could eliminate some of that debt by cashing $35,000 of RRSP assets. A one-time tax at 25%, far less than years of 20% interest on credit card debt, would reduce the net payout to $26,250. They could add $5,400 from their TFSAs to eliminate most of their $35,360 credit card debt. The far less costly line of credit debt, which carries a 4% average interest rate, will be paid off in a few years.

Planning Retirement

They have one rental property with an estimated market value of $325,000. Its $5,200 annual return after its mortgage is paid, which is 7% on their equity of $74,000 would vanish were interest rates to rise on its floating rate note to 5%. They will have no financial assets after they cash out of their TFSAs and RRSPs. Rather than keep the rental property, they could sell it for an estimated $325,000 less selling costs of about $15,000 They could use the net gain of about $60,000 to reduce their home mortgage, Mr. Moran suggests. They would have less debt and could use their line of credit for emergency funds, the planner adds.

When fully retired, Linda and John will have job pensions that add up to $66,753 a year, two CPP cheques that will total $18,924 a year, and two OAS benefits that will total $13,410. The annual grand total, $99,085 will be taxed after pension splits, age and pension credits at an average rate of 17% and leave $6,850 for monthly spending. If they have eliminated $5,500 a month debt service costs on their credit cards and line of credit, sold the rental property, ended carrying charges on the rental property, eliminated property tax on the rental unit and reduced their own home’s mortgage by using money from sale of the rental property, their discretionary income for things they want to spend money on rather than carrying costs they must spend money on will be more in retirement than it is today, Mr. Moran estimates.

“John and Linda can uncomplicate their lives by cleaning up their disastrous finances and using money from sale of the rental property to reduce their own mortgage debt. They will have a comfortable retirement,” Mr. Moran says.

(C) 2014 The Financial Post, Used by Permission